On 13 March 2018 Chancellor Philip Hammond delivered his Spring Statement 2018, this time there was there was no red briefcase, no red book, and on a positive note; no tax changes and, as a result, there was a push towards dealing with potential alterations to the tax system via consultation.

However, it is worth noting that there are changes coming up that were announced/confirmed in the Autumn Budget 2017, and that businesses do need to be aware of. A summary of the key changes are as follows:

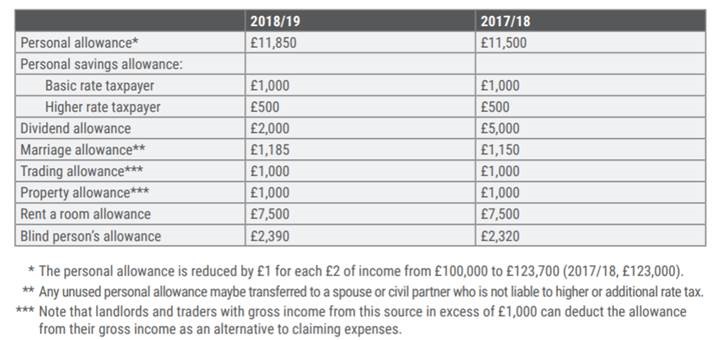

- The tax-free dividend allowance will reduce from £5,000 to £2,000 from 6 April 2018.

- As from 6 April 2018, the minimum employer contribution towards an employee’s workplace pension will increase from 1% to 2%, minimum employee contributions are also increased from the same date. These contributions are generally mandatory for workers aged between 22 and state pension age, earning more than £10,000 a year.

- National minimum wage rates for all ages and apprentices are increasing from 1 April 2018. For 18 to 20-year-olds and 21 to 24-year-olds, National living wages and national minimum wages rates:

- 25 and over – £7.83

- 21-24 – £7.30

- 18-20 – £5.90

- Under 18 – £4.20

- Apprentice – £3.70 – If under 19 or in first year of apprenticeship.

Allowances that reduce taxable income or are not taxable

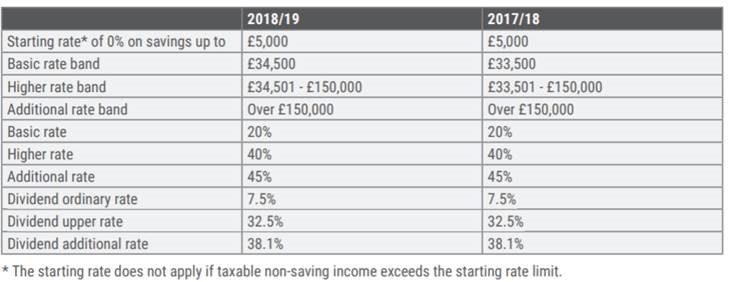

Taxable income bands and tax rates

Note : The above allowances and following bands and rates mean that someone with income (including benefits in kind)/profits of no more than £100K would pay 40% tax on income (including benefits in kind)/profits above £46,851.

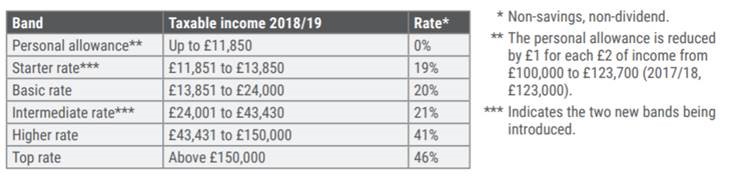

Scotland

The main consultation points announced in The Chancellor’s Spring Statement that relate to business owners are as follows:

Business Rates

The government announced plans at Autumn Budget 2017 to reform the business rates revaluation cycle by increasing the frequency of valuations to every three years following the next revaluation. The chancellor announced at Spring Statement 2018 that the next revaluation of business rates would be brought forward by one year to 2021, four years after the last revaluation. The aim being that ratepayers may benefit from three-year revaluations at the earliest point. It will be based on market rental values on 1 April 2019.

Comment: As ratepayers will only benefit if there is a fall in Business Rates any benefit will only arise if rental values at 1 April 2019 are below those at the last revaluation.

Extension of tax relief for self-funded work related training

Creating a more skilled workforce is one of the key focus points for the government and this has led to a consultation on the extension of tax relief for self-funded training by employees and the self-employed to support improving their skills and retraining.

At present, tax relief for employees or the self-employed who pay for their own training can be highly restricted. This is due to the differentiation between:

- training which maintains or updates existing skill; in which case it allows for tax relief, and

- training which creates new skills; where it does not allow for tax relief.

This consultation is at an early stage and does not specify how to extend the existing scope of tax relief for self-funded, work-related training

VAT Registration Threshold

The Government is concerned that the current design of the VAT registration threshold may be dis-incentivising small businesses from growing their business and improving productivity. Currently if the taxable turnover of a business in a 12-month period exceeds the threshold of £85,000 (until March 2020) the business must register and account for VAT. This call for review is split into three parts:

- how the threshold might currently affect business growth

- the burdens created by the VAT regime at the point of registration, and why businesses might manage their turnover to avoid registering

- the possible policy solutions, based on international and domestic examples

VAT Collection

The Government seeks to ensure a level playing field, by removing any unfair advantage overseas businesses may have over UK businesses. The Government introduced packages of measures at both Budget 2016 and Autumn Budget 2017 to tackle the issue of overseas businesses selling goods to UK consumers without paying the correct UK VAT. In March 2017, HMRC published a call for evidence, seeking views on the feasibility of a ‘split payment’ collection method for VAT as a further step in preventing this type of non-compliance.

A new consultation has been launched on VAT split payment, which seeks to determine steps that could be undertaken to allow VAT to be extracted from overseas sellers. The thrust of the measure will be to harness new technology in the payments industry to collect VAT on online sales in real time and transfer it directly to HMRC. There appears to be little immediate impact for businesses which conduct their trade entirely within the UK, but businesses trading internationally could face additional VAT compliance issues.

Allowing entrepreneurs’ relief on gains made before dilution

It was announced that a consultation would be launched in relation to a possible change to the qualifying conditions for entrepreneurs’ relief. Currently in some cases, an individual may lose eligibility for entrepreneurs’ relief when their company’s fundraising efforts result in their shareholding becoming diluted below 5%. For some businesses this may act as a barrier to growth.

The proposals include a new process by which individuals may remain entitled to entrepreneurs’ relief on gains on shares in, or securities of, a company that relate to the time before the individual’s shareholding became diluted. The Government proposes this may be achieved through:

- allowing individuals to elect to be treated as having disposed of and reacquired their shares at the then market value

- allowing individuals to defer the taxation of this gain until an actual disposal of the shares.

Extension of security deposit legislation

At Autumn Budget 2017, the government announced it would extend existing security deposit legislation to include corporation tax and the construction industry scheme (CIS) deductions from April 2019. This consultation seeks to determine the most effective means of introducing this change.

Businesses, or Directors within a business, with a poor compliance or payment record in relation to corporation tax or CIS may be required to make security deposits. It is worth noting that these measures target businesses that will not, rather than cannot, pay the tax that is due. For those who are struggling, HMRC may allow some flexibility, including time to pay arrangements.

Cash and digital payments

The review aims to find out more about removing barriers to digital payments, to better understand more about the costs and disincentives in making digital payments and what role the government can play in addressing these issues. The Government is using the consultation to determine how it can ensure cash remains accessible, especially for those groups who use cash for legitimate purposes.

The Government is also seeking to determine what more can be done to clamp down on the minority who use cash to evade tax or launder money. As part of this process, the government wishes to review large cash transactions and determine why these are used, plus assess the impact on businesses of adopting the approach taken by other countries to limit these transactions. Such impacts include the consequences for tax compliance.

Tackling the plastic problem

This consultation seeks to explore how changes to the tax system or charges could be used to reduce the amount of single-use plastics wasted. There will also be a focus on driving innovation in this area to achieve similar outcomes. The intention is to review the whole supply chain, from production and retail, through to consumption and disposal.

Enterprise Investment Scheme Knowledge – Intensive Fund

The purpose of this consultation is to aid businesses that have high growth potential but are research and development and capital intensive and, therefore, they may have the most difficulty obtaining the capital they need to scale up.

It attempts to review the possibility of a new enterprise investment scheme fund structure aimed at improving the supply of capital to such companies. There is a need to build the government’s understanding of the capital gap that knowledge-intensive companies face, and the consultation seeks views on the best way of closing that gap.

Corporate Tax and the Digital Economy

The consultation process regarding corporate tax and the digital economy had already closed by Spring Statement 2018. However, an updated position paper was published by the government which highlighted several key points and views from the review.

The participation and engagement of users is an important aspect of value creation for certain digital business models, and is likely to be reflected through several channels, such as the provision of content or as a contribution to certain intangibles such as brand. The preferred and most sustainable solution to this challenge is reform of the international corporate tax framework to reflect the value of user participation.

The above is intended only as a brief summary of the key Autumn Budget 2017 and Spring Statement 2018 announcements and should not be taken as tax advice.

A good Accountant will be happy to explain the pros and cons of Government policy announcements and changes and how they affect you and your business. Here at Keen Dicey Grover our door is always open to talk you through the complexities of tax, allowances and related Government policies.

Our policy is to work closely with our clients to ensure best practice use of business structures to ensure they are operating in the most financially efficient way, now and in the future. By ensuring our clients are confident and informed about their financial business structure, we allow them to concentrate on the key activities of growing their businesses and their finances.

Keen Dicey Grover

We care………..we really care

Recent Comments